David García, Claudio Juan Tessone, Pavlin Mavrodiev, Nicolas Perony.

Journal of the Royal Society Interface, 2014, 11 (99)

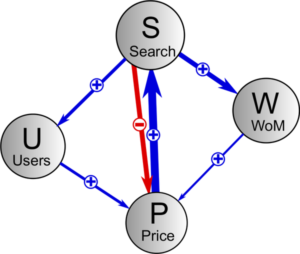

What is the role of social interactions in the creation of price bubbles? Answering this question requires obtaining collective behavioural traces generated by the activity of a large number of actors. Digital currencies offer a unique possibility to measure socio-economic signals from such digital traces. Here, we focus on Bitcoin, the most popular cryptocurrency. Bitcoin has experienced periods of rapid increase in exchange rates (price) followed by sharp decline; we hypothesize that these fluctuations are largely driven by the interplay between different social phenomena. We thus quantify four socio-economic signals about Bitcoin from large datasets: price on online exchanges, volume of word-of-mouth communication in online social media, volume of information search and user base growth. By using vector autoregression, we identify two positive feedback loops that lead to price bubbles in the absence of exogenous stimuli: one driven by word of mouth, and the other by new Bitcoin adopters. We also observe that spikes in information search, presumably linked to external events, precede drastic price declines. Understanding the interplay between the socio-economic signals we measured can lead to applications beyond cryptocurrencies to other phenomena that leave digital footprints, such as online social network usage.

What is the role of social interactions in the creation of price bubbles? Answering this question requires obtaining collective behavioural traces generated by the activity of a large number of actors. Digital currencies offer a unique possibility to measure socio-economic signals from such digital traces. Here, we focus on Bitcoin, the most popular cryptocurrency. Bitcoin has experienced periods of rapid increase in exchange rates (price) followed by sharp decline; we hypothesize that these fluctuations are largely driven by the interplay between different social phenomena. We thus quantify four socio-economic signals about Bitcoin from large datasets: price on online exchanges, volume of word-of-mouth communication in online social media, volume of information search and user base growth. By using vector autoregression, we identify two positive feedback loops that lead to price bubbles in the absence of exogenous stimuli: one driven by word of mouth, and the other by new Bitcoin adopters. We also observe that spikes in information search, presumably linked to external events, precede drastic price declines. Understanding the interplay between the socio-economic signals we measured can lead to applications beyond cryptocurrencies to other phenomena that leave digital footprints, such as online social network usage.