David García, Frank Schweitzer

Royal Society Open Science (2) 150288 (2015)

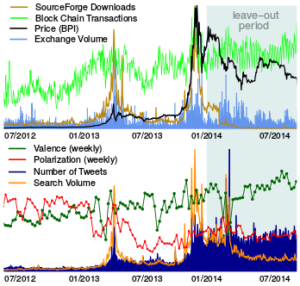

The availability of data on digital traces is growing to unprecedented sizes, but inferring actionable knowledge from large-scale data is far from being trivial. This is especially important for computational finance, where digital traces of human behaviour offer a great potential to drive trading strategies. We contribute to this by providing a consistent approach that integrates various datasources in the design of algorithmic traders. This allows us to derive insights into the principles behind the profitability of our trading strategies. We illustrate our approach through the analysis of Bitcoin, a cryptocurrency known for its large price fluctuations. In our analysis, we include economic signals of volume and price of exchange for USD, adoption of the Bitcoin technology and transaction volume of Bitcoin. We add social signals related to information search, word of mouth volume, emotional valence and opinion polarization as expressed in tweets related to Bitcoin for more than 3 years. Our analysis reveals that increases in opinion polarization and exchange volume precede rising Bitcoin prices, and that emotional valence precedes opinion polarization and rising exchange volumes. We apply these insights to design algorithmic trading strategies for Bitcoin, reaching very high profits in less than a year. We verify this high profitability with robust statistical methods that take into account risk and trading costs, confirming the long-standing hypothesis that trading-based social media sentiment has the potential to yield positive returns on investment.

The availability of data on digital traces is growing to unprecedented sizes, but inferring actionable knowledge from large-scale data is far from being trivial. This is especially important for computational finance, where digital traces of human behaviour offer a great potential to drive trading strategies. We contribute to this by providing a consistent approach that integrates various datasources in the design of algorithmic traders. This allows us to derive insights into the principles behind the profitability of our trading strategies. We illustrate our approach through the analysis of Bitcoin, a cryptocurrency known for its large price fluctuations. In our analysis, we include economic signals of volume and price of exchange for USD, adoption of the Bitcoin technology and transaction volume of Bitcoin. We add social signals related to information search, word of mouth volume, emotional valence and opinion polarization as expressed in tweets related to Bitcoin for more than 3 years. Our analysis reveals that increases in opinion polarization and exchange volume precede rising Bitcoin prices, and that emotional valence precedes opinion polarization and rising exchange volumes. We apply these insights to design algorithmic trading strategies for Bitcoin, reaching very high profits in less than a year. We verify this high profitability with robust statistical methods that take into account risk and trading costs, confirming the long-standing hypothesis that trading-based social media sentiment has the potential to yield positive returns on investment.